2 The framework

This chapter introduces the notation and basic concepts that will be used throughout the book. The chapter is organized into four sections. Section 2.1 starts with a review of unidimensional poverty measurement with particular attention to the well-known FGT measures (Foster, Greer, and Thorbecke 1984) because many methods presented in Chapter 3, as well as the Alkire and Foster (2007, 2011a) measures presented in Chapter 5, are based on FGT indices. Section 2.2 introduces the notation and basic concepts for multidimensional poverty measurement that will be used in subsequent chapters. Section 2.3 delves into the issue of indicators’ scales of measurement, an aspect often overlooked when discussing methods for multidimensional analysis and which is central to this book. Section 2.4 addresses comparability across people and dimensions. Finally Section 2.5 presents in a detailed form the different properties that have been proposed in axiomatic approaches to multidimensional poverty measurement. Such properties enable the analyst to understand the ethical principles embodied in a measure and to be aware of the direction of change they will exhibit under certain transformations.

2.1 Review of Unidimensional Measurement and FGT Measures

The measurement of multidimensional poverty builds upon a long tradition of unidimensional poverty measurement. Because both approaches are technically closely linked, the measurement of poverty in a unidimensional way can be seen as a special case of multidimensional poverty measurement. This section introduces the basic concepts of unidimensional poverty measurement using the lens of the multidimensional framework, so serves as a springboard for the later work. The measurement of poverty requires a reference population, such as all people in a country. We refer to the reference population under study as a

society. We assume that any society consists of at least one observation or unit of analysis. This unit varies depending on the measurement exercise. For example, the unit of analysis is a child if one is measuring child poverty, it is an elderly person if one is measuring poverty among the elderly, and it is a person or—sometimes due to data constraints—the household for measures covering the whole population. For simplicity, unless otherwise indicated, we refer to the unit of analysis within a society as a

person (Chapter 6 and Chapter 7) We denote the number of person(s) within a society by

, such that

is in

or

, where

is the set of positive integers. Note that unless otherwise specified,

refers to the total population of a society and not a sample of it. Assume that poverty is to be assessed using

number of dimensions, such that

. We refer to the performance of a person in a dimension as an achievement in a very general way, and we assume that achievements in each dimension can be represented by a non-negative real valued indicator. We denote the achievement of person

in dimension

by

for all

and

, where

is the set of non-negative real numbers, which is a proper subset of the set of real numbers

.

[30] Subsequently, we denote the set of strictly positive real numbers by

Throughout this book, we allow the population size of a society to vary, which allows comparisons of societies with different populations. When we seek to permit comparability of poverty estimates across different populations, we assume

to denote a fixed set (and number) of dimensions.

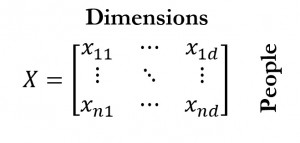

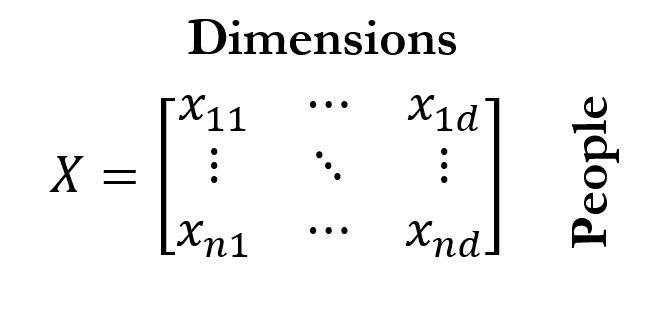

[31] The achievements of all persons within a society are denoted by an

-dimensional achievement matrix

which looks as follows:

We denote the set of all possible matrices of size

by

and the set of all possible achievement matrices by

, such that

. If

, then matrix

contains achievements for

persons in

dimensions. Unless specified otherwise, whenever we refer to matrix

, we assume

. The achievements of any person

in all

dimensions, which is row

of matrix

, are represented by the

-dimensional vector

for all

. The achievements in any dimension

for all

persons, which is column

of matrix

, are represented by the

-dimensional vector

for all

. In the unidimensional context, the

dimensions considered in matrix

—which are typically assumed to be cardinal—can be meaningfully combined into a well-defined overall achievement or resource variable for each person

, which is denoted by

. One possibility, from a welfarist approach, would be to construct each person’s welfare from her vector of achievements using a utility function

.

[32] Another possibility is that each dimension

refers to a different source of income (labour income, rents, family allowances, etc.). Then, one can construct the total income level for each person

as the sum of the income level obtained from each source, that is

. Alternatively, each dimension

can be measured in the quantity of a good or service that can be acquired in a market. Then, one can construct the total consumption expenditure level for each person

as the sum of the quantities acquired at market price, that is

, where

, the price of commodity

is used as its weight. In any of these three cases, the achievement matrix

is reduced to a vector

containing the welfare level or the resource variables of all

persons. In other words, the distinctive feature of the unidimensional approach is not that it necessarily considers only one dimension, but rather that it maps

multiple dimensions of poverty assessment into a

single dimension using a common unit of account.

[33]

2.1.1 Identification of the Income Poor

Since Sen (1976), the measurement of poverty has been conceptualised as following two main steps:

identification of who the poor are and

aggregation of the information about poverty across society. In unidimensional space, the identification of who is poor is relatively straightforward: the poor are those whose overall achievement or resource variable falls below the poverty line

, where the subscript

simply signals that this is a poverty line used in the unidimensional space. Analogous to the construction of the resource variable, the poverty line can be obtained aggregating the minimum quantities or achievements

considered necessary in each dimension. It is assumed that such quantities or levels are positive values, that is

.

[34] These minimum levels are collected in the

-dimensional vector

. If the overall achievement is the level of utility, a utility poverty line needs to be set as

.

[35] On the other hand, when the overall achievement is total income or total consumption expenditure, the poverty line is given by the estimated cost of the basic consumption basket

—or some increment thereof.

[36] Then, given the person’s overall resource value or utility value and the poverty line, we can define the identification function as follows:

identifies person

as poor if

, that is, whenever the resource or utility variable is below the poverty line, and

identifies person

as non-poor if

. We denote the number of unidimensionally poor persons in a society by

and the set of poor persons in a society by

, such that

.

2.1.2 Aggregation of the Income Poor

In terms of aggregation, a variety of indices have been proposed.

[37] Among them, the Foster, Greer and Thorbecke or FGT (1984) family of indices has been the most widely used measures of poverty by international organizations such as the World Bank and UN agencies, national governments, researchers, and practitioners.

[38] For simplicity, we assume the unidimensional variable

to be income. Building on previous poverty indices including Sen (1976) and Thon (1979), the FGT family of indices is based on the normalized income gap—called the ‘poverty gap’ in the unidimensional poverty literature—which is defined as follows: Given the income distribution

, one can obtain a

censored income distribution

by replacing the values above the poverty line

by the poverty line value

itself and leaving the other values unchanged. Formally,

if

and

if

. Then, the normalized income gap is given by:

The normalized income gap of person

is her income shortfall expressed as a share of the poverty line. The income gap of those who are non-poor is equal to 0.

[39] The individual income gaps can be collected in an

-dimensional vector

. Each

element is the normalized poverty gap raised to the power

and it can be interpreted as a measure of

individual poverty where

is a ‘poverty aversion’ parameter. The class of FGT measures is defined as

, thus

can be interpreted as the average poverty in the population. The FGT measures can also be expressed in a more synthetic way as

, where

is the mean operator and thus

denotes the average or mean of the elements of vector

. This presentation of the FGT indices is useful in understanding the AF class (Alkire and Foster 2011a). Within the FGT measures, three measures, associated with three different values of the parameter

, have been used most frequently. The deprivation vector

, for

, replaces each income below the poverty line with 1 and replaces non-poor incomes with 0. Its associated poverty measure

is called the headcount ratio, or the mean of the deprivation vector. It indicates the proportion of people who are poor, also frequently called the incidence of poverty.

[40] The normalized

gap vector

, for

, replaces each poor person’s income with the normalized income gap and assigns 0 to the rest. Its associated measure

, the poverty gap measure, reflects the average depth of poverty across the society. The squared gap

vector

for

, replaces each poor person’s income with the squared normalized income gap and assigns 0 to the rest. Its associated measure—the squared gap or distribution sensitive FGT—is

; it emphasizes the conditions of the poorest of the poor as Box 2.1 explains. The FGT measures satisfy a number of properties, including a subgroup decomposability property that views overall poverty as a population-share weighted average of poverty levels in the different population subgroups.

[41] As noted by Sen (1976), the headcount ratio violates two intuitive principles: (1) monotonicity: if a poor person’s resource level falls, poverty should rise and yet the headcount ratio remains unchanged; (2) transfer: poverty should fall if two poor persons’ resource levels are brought closer together by a progressive transfer between them, and yet the headcount ratio may either remain unchanged or it can even go down. The poverty gap measure satisfies monotonicity, but not the transfer principle; the

measure satisfies both monotonicity and the transfer principle.

[42]

Box 2.1. A numerical example of the FGT measures

A simple example

[43] can clarify the method and these axioms, and will also prove useful in linking the Alkire and Foster methodology (fully described in Chapter 5) to its roots in the FGT class of poverty measures. Consider four persons whose incomes are summarized by vector

and the poverty line is

. The headcount ratio

: Consider first the case of

. Each gap is replaced by a value of 1 if the person is poor and by a value of 0 if non-poor. The deprivation vector is given by:

, indicating that the second and third persons in this distribution are poor. The mean of this vector—the

measure—is one half:

, indicating that 50% of the population in this distribution is poor. Undoubtedly, it provides very useful information. However, as noted by Watts (1968) and Sen (1976), the headcount ratio does not provide information on the depth of poverty nor on its distribution among the poor. For example, if the third person became poorer, experiencing a decrease in her income so that the income distribution became

, the

measure would still be one half; that is, it violates monotonicity. Also, if there was a progressive transfer between the two poor persons, so that the distribution was

, the

measure would not change, violating the transfer principle. This has policy implications. If this was the official poverty measure, a government interested in maximising the impact of resources on poverty reduction would have an incentive to allocate resources to the least poor, that is, those who were closest to the poverty line, leaving the lives of the poorest of the poor unchanged. The poverty gap

(or FGT-1): Here

Each gap is raised to the power

, giving the proportion in which each poor person falls short of the poverty line and

if the person is non-poor. The normalized gap vector is given by

. The

measure is the mean of this vector.

, indicates that the society would require an average of 20% of the poverty line for each person in the society to remove poverty. In fact, $4 is the overall amount needed in this case to lift both poor persons above the poverty line. Unlike the headcount ratio

, the

measure

is sensitive to the depth of poverty and satisfies monotonicity. If the income of the third person decreased so we had

the corresponding normalized gap vector would be

, so

. Clearly,

. Indeed, all measures with

satisfy monotonicity. However, a transfer to an extremely destitute person from a less poor person would not change

, since the decrease in one gap would be exactly compensated by the increase in the other. By being sensitive to the depth of poverty (i.e. satisfying monotonicity), the

measure does make policy makers want to decrease the average depth of poverty as well as reduce the headcount. But because of its insensitivity to the distribution among the poor,

does not provide incentives to target the very poorest, whereas the FGT-2 measure does. The Squared Poverty Gap

(or FGT-2): When we set

, each normalized gap is squared or raised to the power

. The squared gap vector in this case is given by:

. By squaring the gaps, bigger gaps receive higher weight. Note for example that while the gap of the second person (

) is three times bigger than the gap of the third person (

), the squared gap of the second person (

) is nine times bigger than the gap of the third person (

). The mean of the

vector—the

measure—is

. The

measure is sensitive to the depth of poverty: if the income of the third person decreases one unit such that

, the squared gap vector becomes

, increasing the aggregate poverty level to

). It is also sensitive to the distribution among the poor: if there is a transfer of $1 from the third person to the second one, so

becomes

, the squared gap vector becomes

, decreasing the aggregate poverty level to

. Squaring the gaps has the effect of emphasising the poorest poor and providing incentives to policy makers to address their situation urgently. All measures with

satisfy the transfer property

2.2 Notation and Preliminaries for Multidimensional Poverty Measurement

We now extend the notation to the multidimensional context. We represent achievements as

dimensional achievement matrix

, as in the unidimensional framework described in section 2.1. We make two practical assumptions for convenience. We assume that the achievement of person

in dimension

can be represented by a non-negative real number, such that

for all

and

. Also, we assume that higher achievements are preferred to lower ones.

[44] In a multidimensional setting, in contrast to a unidimensional context, the considered

achievements may not be combinable in a meaningful way into some overall variable. In fact, each dimension can be of a different nature. For example, one may consider a person’s income, level of schooling, health status, and occupation, which do not have any common unit of account. As in the unidimensional case, we allow the population size of a society to vary, and we assume

to denote a fixed set (and number) of dimensions.

[45] We denote the set of all possible matrices of size

by

and the set of all possible achievement matrices by

, such that

. If

, then matrix

contains achievements for

persons and a fixed set of

dimensions. Unless specified otherwise, whenever we refer to matrix

, we assume

. The achievements of any person

in all

dimensions, which is row

of matrix

, are represented by the

-dimensional vector

for all

. The achievements in any dimension

for all

persons, which is column

of matrix

, are represented by the

-dimensional vector

for all

. In multidimensional analysis, each dimension may be assigned a weight or deprivation value based on its relative importance or priority. We denote the relative weight attached to dimension

by

, such that

for all

. The weights attached to all

dimensions are collected in a vector

. For convenience we may restrict the weights such that they sum to the total number of considered dimensions, that is:

Alternatively, weights may be normalized; in other words, the weights sum to one:

.

[46]

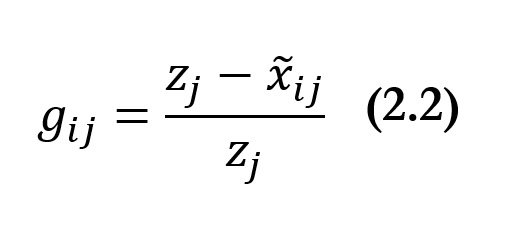

2.2.1 Identifying Deprivations

A common first step in multidimensional poverty assessment in several of the methodologies reviewed in Chapter 3, as well as in the Alkire and Foster (2007, 2011a) methodology, requires defining a threshold in

each dimension. Such a threshold is the minimum level someone needs to achieve in that dimension in order to be non-deprived. It is called the dimensional

deprivation cutoff. When a person’s achievement is strictly below the cutoff, she is considered deprived. We denote the deprivation cutoff in dimension

by

; the deprivation cutoffs for all dimensions are collected in the

-dimensional vector

. We denote all possible

-dimensional deprivation cutoff vectors by

. Any person

is considered deprived in dimension

if and only if

. For several measures reviewed in Chapter 3, and for the AF method, it will prove useful to express the data in terms of deprivations rather than achievements. From the achievement matrix

and the vector of deprivation cutoffs

, we obtain a deprivation matrix

(analogous to the deprivation vector in the unidimensional context) whose typical element

whenever

and

, otherwise, for all

and for all

. In other words, if person

is deprived in dimension

, then the person is assigned a deprivation status value of 1 and 0, otherwise. Thus, matrix

represents the deprivation status of all

persons in all

dimensions in matrix

. Vector

represents the deprivation status of person

in all dimensions and vector

represents the deprivation status of all persons in dimension

. From the matrix

one can construct a deprivation score

for each person

such that

. In words,

denotes the sum of

weighted deprivations suffered by person

.

[47] In the particular case in which weights are equal and sum to the number of dimensions, the score is simply the number of deprivations or deprivation counts that the person experiences. Whenever weights are unequal but sum to the number of dimensions, person

deprivation score

deprivation score is defined as the sum of her weighted deprivation counts. The deprivation scores are collected in an

-dimensional column vector

. On certain occasions, it will be useful to use the deprivation-cutoff-

censored achievement matrix

which is obtained from the corresponding achievement matrix

in

, replacing the non-deprived achievements by the corresponding deprivation cutoff and leaving the rest unchanged. We denote the

th

th element of

by

. Then, formally,

if

and

, otherwise. In this way, all achievements greater than or equal to the deprivation cutoffs are ignored in the censored achievement matrix. When data are cardinally meaningful for all

and all

, and

, in other words, when all the achievements take non-negative values and the deprivation cutoffs take strictly positive values, one can construct dimensional gaps or shortfalls from the censored achievement matrix

as:

[48]

Each

or normalized gap, expresses the shortfall of person

in dimension

as a share of its deprivation cutoff. Naturally, the gaps of those whose achievement

is above the corresponding dimensional deprivation cutoff

are equal to 0. Generalizing the above, the individual normalized gaps can be collected in an

dimensional matrix

where each

element is the normalized gap defined in (2.2) raised to the power

; such normalized gaps can be interpreted as a measure of

individual deprivation in dimension

. When

, we have the

deprivation matrix already defined. When

, we have the

matrix of normalized gaps, and when

, we have the

matrix of squared gaps. Analogous to the FGT measures,

is a deprivation aversion parameter.

2.2.2 Identification and Aggregation in the Multidimensional Case

Sen’s (1976) steps of

identification of the poor and

aggregation also apply to the multidimensional case. It is clear that the identification of who is poor in the unidimensional case is relatively straightforward. The poverty line dichotomizes the population into the sets of poor and non-poor. In other words, in the unidimensional case, a person is poor if she is deprived. However, in the multidimensional context, the identification of the poor is more complex: the terms ‘deprived’ and ‘poor’ are no longer synonymous. A person who is deprived in any particular dimension may not necessarily be considered poor. An identification method, with an associated identification function, is used to define who is poor. We denote the identification function by

, such that

identifies person

as poor and

identifies person

as non-poor. Analogous to the unidimensional case, we denote the number of multidimensionally poor people in a society by

and the set of poor persons in a society by

, such that

. It could be the case that the identification method is based on some ‘exogenous’ variable, in that it is a variable not included in achievement matrix

For example, the exogenous variable could be being beneficiary of some government programme or living in a specific geographic area. One may also define an identification method based on one particular dimension

of matrix

. One may consider the corresponding normative cutoff

to identify the person as poor, in which case the function is

, or one may consider a relative cutoff identifying as poor anyone who is below the median or mean value of the distribution, in which case the function is

. Alternatively, identification may be based on the whole set of achievements not necessarily considering dimensional deprivation cutoffs but rather the relative position of each person on the aggregate distribution

. There are many different ways of identifying the poor in the multidimensional context. A particularly prevalent set of methods consider the person’s vector of achievements and corresponding deprivation cutoffs, such that

identifies person

as poor and

identifies person

as non-poor.

[49] Within this specification of the identification function, at least two approaches can be followed. An approach closely approximating unidimensional poverty is the ‘aggregate achievement approach’, which consists of applying an aggregation function to the achievements across dimensions for each person to obtain an overall achievement value. The same aggregation function is also applied to the dimensional deprivation cutoffs to obtain an aggregate poverty line. As in the unidimensional case, a person is identified as poor when her overall achievement is below the aggregate poverty line. Another method, which we refer to as ‘censored achievement approach’, first applies deprivation cutoffs to identify whether a person is deprived or not in each dimension and then identifies a person considering only the deprived achievements. The ‘counting approach’ is one possible censored achievement approach, which identifies the poor according to the number (count) of deprivations they experience. Note that ‘number’ here has a broad meaning as dimensions may be weighted differently. Chapter 4 and the AF method (Ch 5-10) use a counting approach. When the scale of the variables allows, other identification methods could be developed using the information on the deprivation gaps.

In counting identification methods, the criterion for identifying the poor can range from ‘union’ to the ‘intersection’. The union criterion identifies a person as poor if the person is deprived in

any dimension, whereas the intersection criterion identifies a person as poor only if she is deprived in

all considered dimensions. In between these two extreme criteria there is room for intermediate criteria. Many counting-based measurement exercises since the mid-1970s have used intermediate criteria (see Chapter 4). The AF methodology formally incorporated it into an axiomatic framework.

[50] Once the identification method has been selected, the aggregation step requires selecting a poverty index, which summarizes the information about poverty across society. A poverty index is a function

that converts the information contained in the achievement matrix

and the deprivation cutoff vector

into a real number. We denote a poverty index as

. An identification and an aggregation method that are used together constitute what we call a multidimensional poverty methodology, and we denote it as

. It will prove useful to introduce notation for two further partial indices related to the overall poverty index

. Each of them offers information on different ‘slices’ of the achievement matrix

as analysed by the corresponding multidimensional poverty methodology

; that is, the partial indices are dependent on the selected identification and aggregation methods. One of these partial indices is the poverty level of a particular subgroup within the total population, denoted as

, where

is the achievement matrix of this particular subgroup

(which could be people of a particular ethnicity, for example) contained in matrix

. Visually, this partial index is based on a horizontal slice of the achievement matrix

(i.e. a set of rows). The other partial index is a function of the

post-identification dimensional deprivations, denoted as

, where, as stated above, vector

represents the achievements in dimension

for all

persons and

is the deprivation cutoffs vector.

[51] This is precisely why the full vector of deprivation cutoffs

is an argument of the index and not just the particular deprivation cutoff

. Recall that under some identification methods, it is possible to have some people who experience deprivations but are not identified as poor (for example, when a counting approach is used with an identification strategy that it is not union). In such cases, their deprivations will not be considered in the poverty measure and therefore will not be considered in this partial index either. In a visual way, this partial index is based on a vertical slice of the achievement matrix

(i.e. a column). These two partial indices will be used when introducing the different principles of multidimensional poverty measures in section 2.5.3. As we shall see, although identification and aggregation have, since Sen (1976), usually been recognized as key steps in poverty measurement, some methods in the multidimensional context do not follow these steps. We will clarify this in Chapter 3.

2.2.3 The Joint Distribution

Throughout this book we will frequently refer to the

joint distribution in contrast to the

marginal distribution and we will also use the expression

joint deprivations. The concept of a joint distribution comes from statistics where it can be represented using a joint cumulative distribution function.

[52] The relevance of the joint distribution in multidimensional analysis was articulated by Atkinson and Bourguignon (1982), who observed that multidimensional analysis was

intrinsically different because there could be identical dimensional marginal distributions but differing degrees of interdependence between dimensions.

[53] In this book we treat the achievement matrix

as a representation of the joint distribution of achievements. Each row contains the (vector of) achievements of a given person in the different dimensions, and each column contains the (vector of) achievements in a given dimension across the population. From that matrix, considered with deprivation cutoffs, it is possible to obtain the proportion of the population who are simultaneously deprived in different subsets of

dimensions. In other words, it is possible to obtain the proportion of people who experience each possible profile of deprivations. This is visually clear in the deprivation matrix

, which represents the joint distribution of deprivations. The higher order matrices

and

obviously offer further information regarding the joint distribution of the depths of deprivations. The importance of considering the joint distribution of achievements, which in turn enables us to look at joint deprivations, is best understood in contrast with the alternative of looking at the

marginal distribution of achievements, and, thus, the

marginal deprivations. The marginal distribution is the distribution in one specific dimension without reference to any other dimension.

[54] The marginal distribution of dimension

is represented by the column vector

. From the marginal distribution of each dimension, it is possible to obtain the proportion of the population deprived with respect to a particular deprivation cutoff. However, by looking at only the marginal distribution, one does not know who is simultaneously deprived in other dimensions.

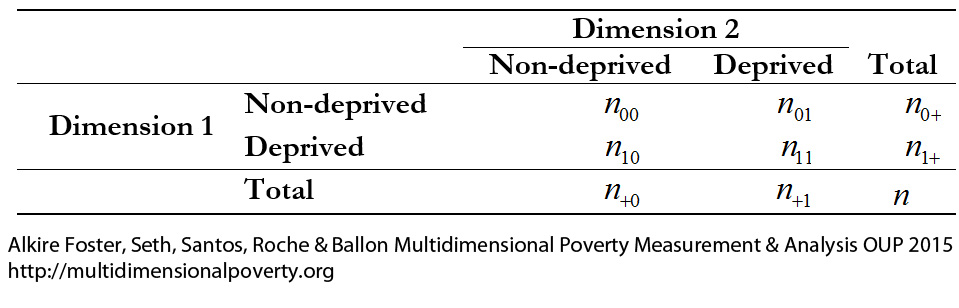

[55] Table 2.1 illustrates the relevance of the joint distribution in the basic case of

persons and

dimensions using a contingency table.

Table 2.1. Joint distribution of deprivation in two dimensions

We denote the number of people deprived and non-deprived in the first dimension by

and

, respectively; whereas, the number of people deprived and non-deprived in the second dimension are denoted by

and

, respectively. These values correspond to the marginal distributions of both dimensions as depicted in the final row and final column of the table. They could equivalently be expressed as proportions of the total, in which case, for example, (

) would represent the proportion of people deprived (or the headcount ratio) in Dimension 1. The marginal distributions, however, do not provide information about the joint distribution of deprivations, which is described in the four internal cells of the table. In particular, the number of people deprived in both dimensions is denoted by

, the number of people deprived in the first but not the second dimension is denoted by

, and the number of people deprived in the second and not in the first dimension is denoted by

. We know that

people are deprived in both dimensions and the sum of

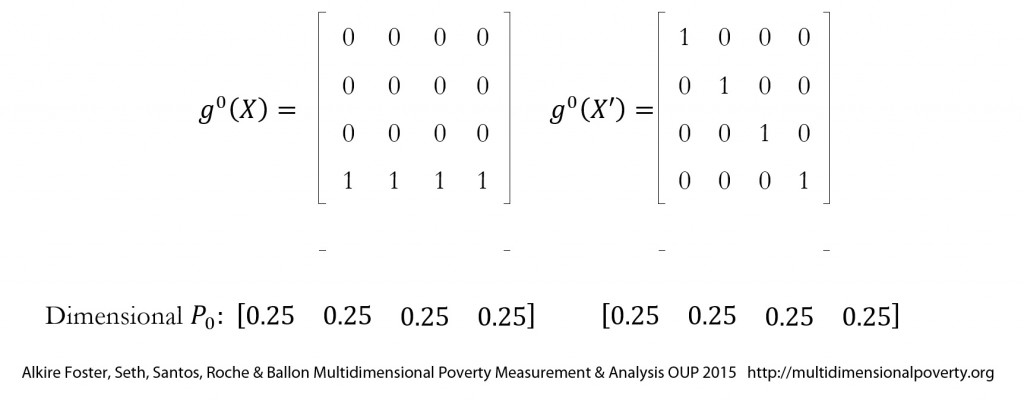

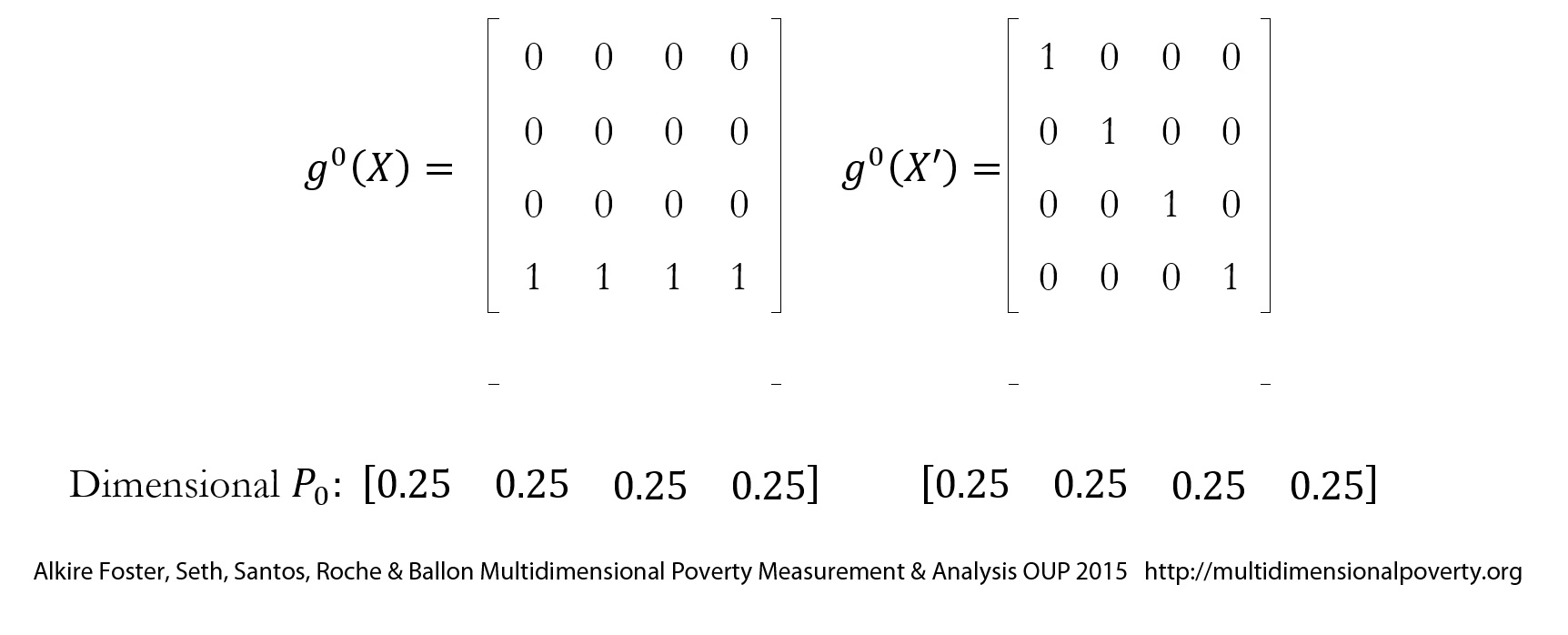

is the number of people deprived in at least one dimension. These values correspond to the joint distribution of deprivations. Consider now the case of four dimensions and four people, to see how valuable information can be added by the joint distribution. Table 2.2

[56] presents the deprivation matrix

of two hypothetical distributions,

and

. Such a matrix presents joint distributions of deprivations in a compact way and is used regularly throughout this book.

Table 2.2. Comparison of two joint distributions of deprivations in four dimensions

In the table, the marginal distributions of each dimension’s

are identical in deprivation matrices

and

. Thus, the proportions of people deprived in each dimension are the same in the two distributions (25%). Yet, while, in distribution

one person is deprived in all dimensions and three people experience zero deprivations, in distribution

, each of the four persons is deprived in exactly one dimension. In other words, although the marginal distributions are identical, the two joint distributions

and

are very different. We understand that multiple deprivations that are

simultaneously experienced are at the core of the concept of multidimensional poverty, and this is the reason why the consideration of the joint distribution is important. However, as we shall see, not all methodologies consider the joint distribution. In the next section, we introduce the notation for two methodologies of this type.

2.2.4 Marginal Methods

Some of the methods for multidimensional poverty assessment introduced in Chapter 3 can be called

marginal methods because they do not use information contained in the joint distribution of achievements. In other words, they ignore all information on links across dimensions. Following Alkire and Foster (2011b), a marginal method assigns the same level of poverty to any two matrices that generate the same marginal distributions. In Table 2.2, a marginal method would assign the same poverty level to distribution

(four deprivations are experienced by one person) and distribution

(each person experiences exactly one deprivation). That is, it would not be able to show whether the deprivations are spread evenly across the population or whether they are concentrated in an underclass of multiply deprived persons. Such marginal methods can also be linked to the order of aggregation while constructing poverty indices (Pattanaik et al 2012). Specifically, a measure can be obtained by first aggregating achievements or deprivations across people (column-first) within each dimension and then aggregating across dimensions, or it can be obtained by first aggregating achievements or deprivations for each person (row-first) and then aggregating across people. Only measures that follow the second order of aggregation (i.e., first across dimensions for each person and then across persons) reflect the joint distribution of deprivations (Alkire 2011: 61, Figure 7). Measures that follow the first order of aggregation fall under marginal methods of poverty measurement.

Marginal methods also include cases where achievements for different dimensions are drawn from

different data sources and/or from

different reference groups within a population—as occurred, for example, in many indicators associated with the Millennium Development Goals (MDGs). In this case, rather than having an

dimensional matrix

of achievements, one may have a ‘collection’ of vectors

, representing the achievements of

people in dimension

for all

. Note that each

vector may refer to

different sets of people such as children, adults, workers, or females, to mention a few. Suppose as before, that a deprivation cutoff

is defined. Then, we define a

dimensional deprivation index

for dimension

by

, which assesses the deprivation profile of

people in dimension

. The deprivation index might be simply the percentage of people who are deprived in this indicator or some other statistic such as child mortality rates. Note that deprivations are clearly identified in each dimension; however, because the underlying columns of dimensional achievements are not linked, no decision on who is to be considered multidimensionally poor can be made. This is a key difference between the dimensional deprivation index

and the post-identification dimensional deprivation index

which depends on the entire deprivation cutoff vector

(and not just

) and thus captures the joint distribution of deprivations (see Section 2.2.2). Different dimensional deprivation indices

can be considered in a set, constituting the ‘dashboard approach’, or combined by some aggregation function, what is often called a ‘composite index’ (Chapter 3).

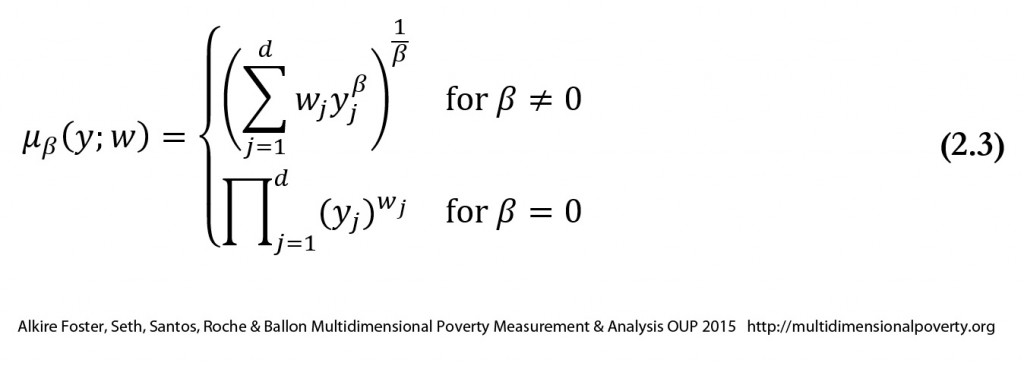

2.2.5. Useful Matrix and Vector Operations

Throughout the book, we use specific vector and matrix operations. This section introduces the technical notation covering vectors and matrices. We denote the transpose of any matrix

by

where

has the rows of matrix

converted into columns. Formally, if

and the

th element of

is written

, then

, where

is the

th element of

for all

and

. The same notation applies to a vector, with

being the transpose of

. Thus, if

is a row vector,

is a column vector of the same dimension. As stated in section 2.1 the average or mean of the elements of any vector

is denoted by

, where

. Similarly, the average or mean of the elements of any matrix

is denoted by

, where

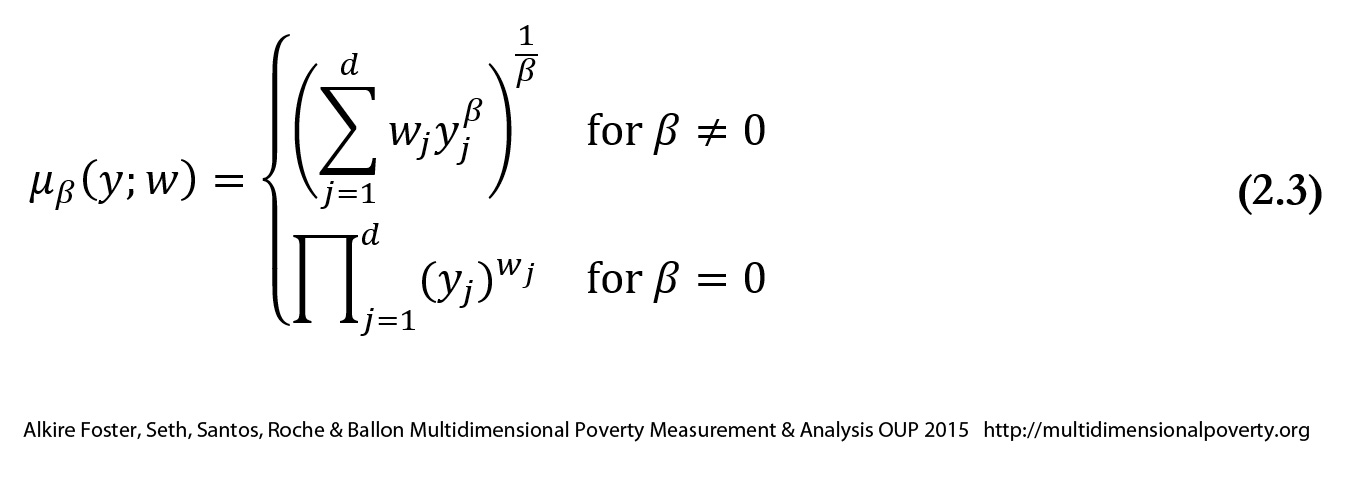

. Later in the book we use a related expression, the so-called ‘generalized mean of order’

. Given any vector of achievements

, where

, the expression of the weighted generalized mean of order

is given by

where

and

. When weights are equal,

for all

. Each generalized mean summarizes distribution

into a single number and can be interpreted as a ‘summary’ measure of well- or ill-being, depending on the meaning of the arguments

. When

for all

, we write

simply as

. When

,

reduces to the arithmetic mean and is simply denoted by

When

, more weight is placed on higher entries and

is higher than the arithmetic mean, approaching the maximum entry as

tends to

. For

more weight is placed on lower entries, and

is lower than the arithmetic mean, approaching the minimum entry as

tends to

. The case of

is known as the geometric mean and

as the harmonic mean

. Expression (2.3) is also known as a constant elasticity of substitution function, frequently used as a utility function in economics. When generalized means are computed over achievements, it is natural to restrict the parameter to the range of

giving a higher weight to lower achievements and penalizing for inequality (Atkinson 1970). Likewise when generalized means are computed over deprivations, it is natural to restrict the parameter to the range of

giving a higher weight to higher deprivations and also penalizing for inequality. Box 2.2 contains an example of generalized means.

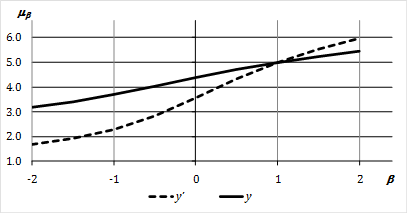

Box 2.2. Example of generalized Means[57]

Consider two distributions

and

with the following distribution of achievements in a particular dimension:

and

. We first show how to calculate

for certain values of

and then compare two distributions with a graph where

ranges from

to

. In this example, we assume that all dimensions are equally weighted:

.

Arithmetic Mean:The arithmetic mean (

) of distribution

is:

.

Geometric Mean:If

, then

is the ‘geometric mean’ and by the formula presented in (2.3) can be calculated as:

.

Harmonic Mean: If

, then

is the harmonic mean and can be calculated as:

. The following graph depicts the values of the

of

and

for different values of

. Note that

when

, given that the two distributions have the same arithmetic mean. In both cases, when

, the generalized means are strictly lower than the arithmetic mean, because the incomes are unequally distributed. Note moreover that for this range,

because

has a more unequal distribution. On the other hand, for

,

as the higher incomes receive a higher weight.

Another matrix transformation that we use is

replication. A matrix is a replication of another matrix if it can be obtained by duplicating the rows of the original matrix a finite number of times. Suppose the rows of matrix

are replicated

number of times, where

. Then the corresponding replication matrix is denoted by

. notation may be used for replication of any vector

:

. We do not consider column replication, as we consider a fixed set of dimensions. Analogous We also use three types of matrices associated with particular operations: a

permutation matrix, a

diagonal matrix, and a

bistochastic matrix. A permutation matrix, denoted by

, is a square matrix with one element in each row and each column equal to 1 and the rest of the elements equal to 0. Thus the elements in every row and every column sum to one. We eliminate the special case when a permutation matrix is an ‘identity matrix’ with the diagonal elements equal to 1 and the rest equal to 0. What does a permutation matrix do? If any matrix

is pre-multiplied by a permutation matrix, then the rows of matrix

are shuffled without their elements being altered. Similarly, if any matrix

is post-multiplied by a permutation matrix, then the columns of

are shuffled without their elements being altered.

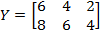

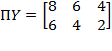

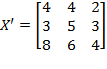

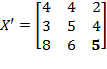

Example of Permutation Matrix: Let

. Consider

. Then

. Thus, the rows of

are merely swapped. Similarly, consider

. Then

. Note that the second and the third columns have swapped their positions. The first column did not change its position because the first diagonal element in

is equal to one.

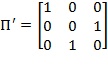

A diagonal matrix, denoted by

, is a square matrix whose diagonal elements are not necessarily equal to 0 but all off-diagonal elements are equal to 0. Let us denote the

th element of

by

. Then,

for all

. For our purposes, we require the diagonal elements of a diagonal matrix to be strictly positive or

. What is the use of a diagonal matrix? If any matrix

is post-multiplied by a diagonal matrix, then the elements in each column are changed in the same proportion. Note that different columns may be multiplied by different factors.

Example of Diagonal Matrix: Let

. Consider

. Then

. Each element in the first column has been halved and each element in the third column has been doubled. However, the second column did not change because the corresponding element of

is equal to one.

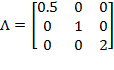

A bistochastic matrix, denoted by

, is a square matrix in which the elements in each row and each column sum to one. If the

th element of

is denoted by

, then

for all

and

for all

. Why do we require a bistochastic matrix? If a matrix is pre-multiplied by a bistochastic matrix, then the variability across the elements of each column is reduced while their average or mean is preserved. Note that if a diagonal element in a bistochastic matrix is equal to one, the achievement vector of the corresponding person remains unaffected. If the bistochastic matrix is a permutation matrix or an identity matrix, then the variability remains unchanged.

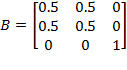

Example of Bistochastic Matrix: Let

. Consider

. Then

. The bistochastic matrix equalizes the achievements across its elements.

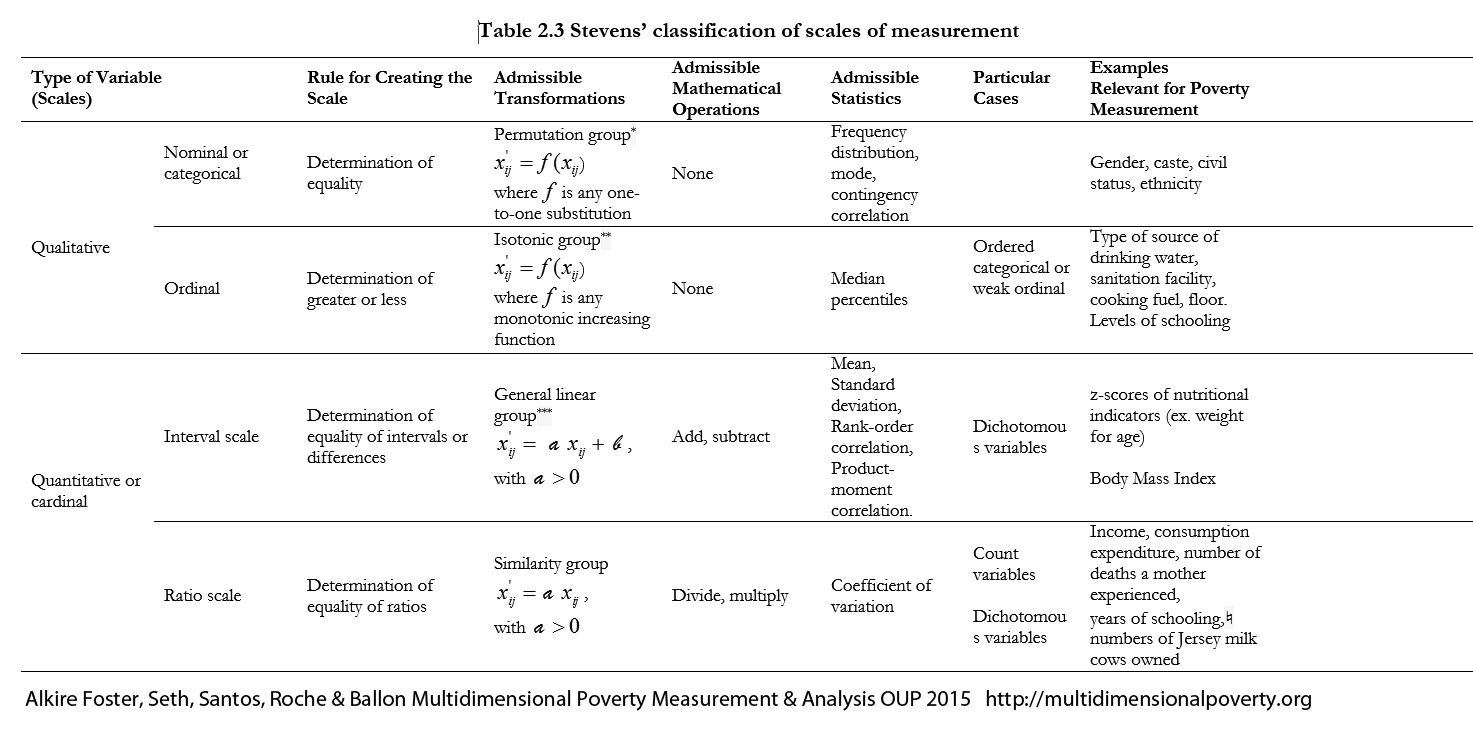

2.3 Scales of Measurement: Ordinal and Cardinal Data

An important element of the framework in multidimensional poverty measurement relates to the scales of measurement of the indicators used. Scales of measurement are key because they affect the kind of

meaningful operations that can be performed with indicators. In fact, as we will observe, certain types of indicators may not allow a number of operations and thus cannot be used to generate certain poverty measures. What does

scale of measurement refer to exactly? Following Roberts (1979) and Sarle (1995), we define a scale of measurement to be a particular way of assigning numbers or symbols to assess certain aspects of the empirical world, such that the relationships of these numbers or symbols replicate or represent certain observed relations between the aspects being measured. There are different classifications of scales of measurement. In this book, we follow the classification introduced by Stevens (1946) and discussed in Roberts (1979). Stevens’ classification is consistent with Sen (1970, 1973), which analysed the implications of scales of measurement for welfare economics, distributional analysis, and poverty measurement, and it has largely stood the test of time.

[58] Stevens’ (1946) classification relies on four key concepts: assignment rules, admissible transformations, permissible statistics, and meaningful statements. First, the defining feature of a scale is the

rule or basic empirical operation that is followed for assigning numerals, as elaborated below. Second, each scale has an associated set of

admissible mathematical transformations such that the scale is preserved. That is, if a scale is obtained from another under an admissible transformation, the rule under the transformed scale is the same as under the original one. Third, a

permissible statistic

refers to a statistical operation that when applied to a scale, produces the same result as when it is applied to the (admissibly) transformed scale. While the word ‘permissible’

may sound rather strong, it is justifiable under the premise that ‘one should only make assertions that are invariant under admissible transformations of scale’ (Marcus-Roberts and Roberts 1987, 384).

[59] Fourth, a statement is called

meaningful if it remains unchanged when all scales in the statement are transformed by admissible transformations (Marcus-Roberts and Roberts 1987: 384).

[60] Stevens (1946) considered four basic empirical operations or rules that define four types of scales: equality, rank-order, equality of intervals, and equality of ratios. Following them, he defined four main types of scales: nominal, ordinal, interval, and ratio. Stevens' classification is not exhaustive. For example, it only applies to scales that take real values and which are regular.

[61] Also, note that alternative terms are sometimes used for some of Stevens’ types. For example, nominal scales are sometimes referred to as categorical scales. Table 2.3 lists the scale types mentioned above from ‘weakest’ to ‘strongest’ in the sense that interval and ratio scales contain much more information than ordinal or nominal scales. The column that presents the rule defining each scale type is cumulative in the sense that a rule listed for a particular scale must be applicable to the scales in rows preceding it. The column that lists the permissible statistics is also cumulative in the same sense. In contrast, the column that lists the admissible transformations goes from general to particular: the particular operation listed in a row is included in the operation listed above. We now introduce each scale ‘type’. The scale pertains to an indicator used to measure dimension

. The term ‘indicator

’ denotes the indicator of dimension

. Achievements in indicator

across the population are represented by vector

, where

is the achievement of person

in the

indicator. Indicator

is said to be

nominal or

categorical if the scale is based on mutually exclusive categories, not necessarily ordered. Nominal variables are frequently called

categorical variables. The rule or basic empirical operation behind this type of scale is the determination of equality among observations. A nominal scale is ‘the most unrestricted assignment of numerals. The numerals are used only as labels or type numbers, and words or letters would serve as well’ (Stevens 1946: 678). That is, numbers assigned to the various achievement levels in this domain are simply placeholders. Stevens introduces two common types of nominal variables. One uses ‘numbering’ for identification, such as the identification number of each household in a survey or the line number of individuals living within a household. The other uses numbering for a classification, such that all members of a social group (ethnic, caste, religion, gender, or age) or geographical regions (rural/urban areas, states, or provinces) are assigned the same number. The first type of nominal variable is simply a particular case of the second. There is a wide range of admissible transformations for this type of scale. In fact, any transformation that substitutes or permutes values between groups, that is, any one-to-one substitution function

such that

for all

, will leave the scale form invariant. Given that in a nominal variable, the different categories do not have an order, neither arithmetic operations nor logical operations (aside from equality) are applicable. In terms of relevant statistics, if the nominal variable is simply an identifier, then only the number of categories is a relevant statistic; if the nominal variable contains several cases in each category, then the mode and contingency methods can be implemented, as can hypotheses tests regarding the distribution of cases among the classes (Stevens 1946: 678–9). Indicator

is said to be

ordinal if the order matters but not the differences between values. The rule or basic empirical operation behind this type of scale is the determination of a rank order. Categories can be ordered in terms of ‘greater’, ‘less’, or ‘equal’ (or ‘better’, ‘worse’, ‘preferred’, ‘not preferred’). Admissible transformations consist of any order-preserving transformation, that is, any strictly monotonic increasing function

such that

for all

, as these will leave the scale form invariant. Thus, admissible transformations include logarithmic operation, square root of the values (nonnegative), linear transformations, and adding a constant or multiplying by another (positive) constant. Examples of ordinal scales are preference orderings over various categories, or subjective rankings. Given that the true intervals between the scale points are unknown, arithmetic operations are meaningless (because results will change with a change of scale), but logical operations are possible. For example, we can assert that someone reporting a health level of four feels ‘better’ than someone reporting a health level of ‘three’, who in turn feels better than a ‘two’, but we cannot assert whether the difference between level three and four is the same as the difference between level two and three. Nevertheless, some statistics are applicable to ordinal variables, namely, the number of cases, contingency tables, the mode, median, and percentiles.

[62] Statistics such as mean and standard deviation cannot be used. Clearly, an ordinal variable is a nominal variable but the converse is not true. Ordinal and nominal (or categorical) variables are also sometimes referred to as qualitative variables.

Unordered categorical variables—such as eye colour—are not relevant for the construction of poverty measures. Relevant categorical variables are those that can be exhaustively and non-trivially partitioned into at least two sets according to some exogenous condition, and in which those sets can be arranged in a complete ordering. There will be fewer sets than there are categorical responses, or else the original variable would already have been ordinal. If a set contains multiple elements, it may not be possible to rank those elements against one another. Hence the resulting construction would be a ‘semi-order’ (Luce 1956) or ‘quasi-order’ (Sen 1973). Additionally, it may be possible to distinguish set(s) that are considered to be adequate achievements from those that are inadequate, forming a ‘weak order’, that is, some pairs of responses can be ranked as ‘preferred to’ and some others cannot be ranked.

[63] For example, because it is difficult to assess whether it is better to have access to a public tap than to a borehole or a protected well as sources of drinkable water, the Millennium Development Goal indicator considers all three of them to be adequate sources of drinkable water (unrankable). Similarly, while one cannot rank access to an unprotected spring versus access to rainwater, both sources are considered inadequate by MDG standards. A variable thus constructed is often called an ‘ordered categorical’; we might also call the variables obtained as a weak order of categories in a nominal variable, a ‘weak-ordinal’ variable. Admissible transformations of weak ordinal variables include any transformations that partition the categorical variables into the relevant sets (safe water sources) in the same order; any apparent ordering of elements within the relevant sets can vary freely. Indicator

is said to be of

interval scale if the rule or basic empirical operation behind its scale is the determination of equality of intervals or differences. Importantly, interval scales do not have a predefined zero point. The admissible transformations of interval scale consist of the linear transformation

(with

), as this preserves the differences between categories. While the

difference between two values of an interval-scale variable is meaningful, the ratios are not. The most cited example in this literature refers to two temperature scales: Celsius (

oC) and Fahrenheit (

oF). While the difference between 15

oC and 20

oC is the same as the difference between 20

oC and 25

oC, one cannot say that 20

oC is twice as hot as 10

oC because 0

oC does not mean ‘no temperature’. That is, the Celsius scale (and Fahrenheit scale) lack a natural zero. Also, the difference between 15

oC and 20

oC and between 20

oC and 25

oC is also precisely the same if measured in Fahrenheit (59

oF and 68

oF vs

. 68

oF and 77

oF) although the value of the difference is nine rather than five degrees. An interval scale allows addition and subtraction and the computation of most statistics, namely, number of cases, mode, contingency correlations, median, percentiles, mean, standard deviation, rank-order correlation, and product-moment correlation, but it is not meaningful to compute the coefficient of variation or any other ‘relative’ measure. In multidimensional poverty measurement, one indicator that is usually of interest is the z-score of under 5-year-old children’s nutritional achievement. We consider a nutritional z-score to be of interval-scale type. Box 2.3 provides a more detailed explanation of how to compute z-scores. Z-scores range from negative to positive values, spaced in (the reference population’s) standard deviation units, and the zero value means that the child’s nutritional achievement is at the median of what is considered a healthy population. Indicator

is said to be of

ratio scale if the rule or basic empirical operation behind its scale is the determination of equality of ratios. Such a rule requires the scale to have a ‘natural zero’, namely the value 0 means ‘no quantity’ of that indicator. In other words, the value 0 is the absolute lowest value of the variable. Admissible transformations of interval-scale variables consist of functions such as

(with

), as this preserves the ratio differences. Examples of ratio-scale variables are age, height, weight, and temperature in Kelvin, as 0

o Kelvin means ‘no temperature’; 200 pounds is twice as much as 100 pounds, sixty years as thirty years and so on. Ratio-scale variables allow statements such as ‘a value is twice as large as another’, and they allow any type of mathematical operation, as well as the computation of any statistic (number of cases, mode, contingency correlations, median, percentiles, mean, standard deviation, rank-order correlation, product-moment correlation, and coefficient of variation). Interval- and ratio-scale variables constitute what are commonly referred to as

cardinal variables. It is interesting to observe that in the order presented, from nominal to ratio scales, the admissible transformations become more restricted but the meaningful statistics become more unrestricted, ‘suggesting that in some sense the data values carry more information’ (Velleman and Wilkinson 1993: 66). Stevens (1959, 24) provided an insightful example of how measurement can progress from weaker to stronger scales. Early humans probably could only distinguished between cold and warm and thus used a nominal scale. Later, degrees of warmer and colder had been introduced and so the use of an ordinal scale gained prominence. The introduction of thermometers led to the use of an interval scale. Finally, the development of thermodynamics led to the ratio scale of temperature by introducing the Kelvin scale.

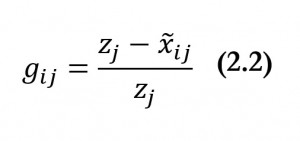

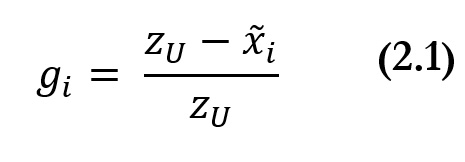

Box 2.3. Children’s nutritional z-scores

The nutritional status of children under 5 years old is assessed with three anthropometric indicators: weight-for-age, also called ‘underweight’; weight-for-height, also called ‘wasting’; and height-for-age, also called ‘stunting’. The indicators are constructed as follows. The World Health Organization has measured the height and weight of a reference population of children from different ethnicities, which is considered to constitute a standard of well nourishment (WHO 2006). From that population, a distribution of weights according to each age, a distribution of heights according to each age, and a distribution of height according to each weight are obtained. Each of these are discriminated by gender. How is a child’s nutrition assessed? Let us consider the case of the weight-for-age (

) indicator. Once the weight and age of the child have been documented, this information can be expressed in her weight-for-age z-score. This is computed as the child’s observed weight minus the median weight of children of the same sex and age in the reference population, divided by the standard deviation of the reference population. That is:

where

is the z-score of weight-for-age,

is the observed weight of child

,

is the median weight of children of the same sex and age as child

in the reference population (healthy children), and

is the standard deviation of the weight of children of that age in the reference population. The z-scores for weight-for-height (

) and height-for-age (

) are computed in an analogous way. Thus,

for all

and all

,

and

. Thus, for example, suppose 14-month-old Anna weighs 8.3 kilograms. The median weight in the reference population of children of that age is 9.4 and the standard deviation is 1.

* Thus, the z-score of Anna is

, meaning that Anna is about one standard deviation below the median weight of healthy children. It is considered that children with z-scores that are more than two standard deviations below the median of the reference population suffer moderate undernutrition, and, if their z-score is more than three standard deviations below, they suffer severe undernutrition (underweight, wasting, or stunting, correspondingly). Children with a z-score of weight-for-height above

standard deviations above the median are considered to be overweight (WHO 1997). An alternative way to assess the nutritional status of children is to use percentiles rather than z-scores, but z-scores present a number of advantages. Most importantly, they can be used to compute summary statistics such as a mean and standard deviation, which cannot be meaningfully done with percentiles (O’Donnell et al. 2008). Note that if we take a linear transformation of the z-score for weight-for-age such that

, where

and

, then

. Note that the difference

(or

) has the same implication as the difference

. This equivalence would hold for any linear transformation, exhibiting the characteristics of an interval-scale indicator.

*These values were taken from WHO’s reference tables: http://www.who.int/childgrowth/standards/sft_wfa_girls_z_0_5.pdf

Having introduced the scales of measurement, it is worth making a few clarifications regarding other frequently-mentioned types of indicators. First, Stevens' classification makes no reference to

continuous versus

discrete variables, for example. Continuous variables can take any value on the real line within a range. Discrete variables, in contrast, can only take a finite or countably infinite number of values.

[64] Ordinal variables are discrete variables, but cardinal ones (interval and ratio scale) can be either discrete or continuous.

[65] Second, note that

count variables such as counts of publications, number of children in a household, or number of chickens, are particular cases of ratio-scale variables (Stevens 1946), such that the only admissible transformation is the identity function, i.e.

. Roberts (1979) refers to the counting scale type as an

absolute scale. Third,

dichotomous (also called binary) variables can be of different scales, depending on the meaning of their categories. When the two values simply refer to unordered, mutually exclusive categories, such as being male or female, the variable is of nominal scale. When there is an order between the categories, such as being deprived or not in a specific dimension, the variable is

cardinal. If the two values refer to having or lacking the same thing, such as a fully functional method for wood smoke ventilation, the variable may be interpreted as of ratio scale.

[66] Fourth, the reader may wonder where do

Likert scales—introduced by Likert (1932) and often used in social sciences—fit? Likert scales are obtained from responses to a set of (carefully phrased) statements to which each respondent expresses her level of agreement on a scale such as one to five: strongly disagree, disagree, neutral, agree, or strongly agree. Each statement and its responses are known as a Likert item. A Likert scale is obtained by summing or averaging the responses to each item so that a score is acquired for each person. Likert scales are frequently treated as interval scales, under the assumption (at times empirically verified) that there is an equal distance between categories (Brown 2011; Norman 2010). Thus, descriptive statistics (like means and standard deviations) and inferential statistics (like correlation coefficients, factor analysis, and analysis of variance) are regularly implemented with Likert scales. However, this has been criticized as being ‘illegitimate to infer that the intensity of feeling between ‘strongly disagree’ and ‘disagree’ is equivalent to the intensity of feeling between other consecutive categories on the Likert scale’ (Cohen et al. 2000, cited in Jamieson 2004: 1217). Thus, there is ongoing disagreement about whether Likert scales should be treated as ordinal scales (Pett 1997; Hansen 2003; Jamieson 2004). Often empirical psychometric tests are performed to ‘verify’ whether the assumption that the scale can be treated as cardinal holds for a particular dataset.

Stevens’ (1946) landmark work sparked a body of literature on measurement theory, which raised strong warnings regarding the applicability of statistics to different scales, including Stevens (1951, 1959), Luce (1959), and Andrews et al. (1981). This engendered an extensive and on-going debate across literatures from psychology to statistics. Some social scientists and statisticians consider that, although, in theory, certain statistics such as the mean and standard deviations are inappropriate for ordinal data, they can still be ‘fruitfully’ applied if the problem in question and data structure (and comparability, if relevant) have been tested and seem to warrant assumptions that they can be treated as interval scale. The arguments in favour of this position are interestingly articulated by Velleman and Wilkinson (1993). For example, it is stated that ‘the meaningfulness of a statistical analysis depends on the questions it is designed to answer’ (Lord 1953, Guttman 1977), that in the end ‘every knowledge is based on some approximation’ (Tukey 1961), and that ‘…if science was restricted to probably meaningful statements it could not proceed’ (Velleman and Wilkinson 1993). Another argument is that parametric methods are highly robust to violation of assumptions and thus can be implemented with ordinal data (Norman 2010). Although we acknowledge this on-going debate, in what follows we do endorse the requirement of meaningfulness—as defined above—in order to compute statistics or mathematical measures in each scale type; hence, we limit the operations with ordinal data to those that cohere with its definition and point out deviations from this. As this section suggests, the indicators’ scale and the analysts’ considered response to scales of measurement must be articulated before selecting a methodology to measure and assess multidimensional poverty. In Chapter 3, we clarify whether each method surveyed can be used with ordinal data. In general, when an indicator is of ratio scale, such as income, consumption, or expenditure (all expressed in monetary units), arithmetic operations with elements of the scale are permissible. Thus, it is meaningful to compute the normalized deprivation gaps as defined in Expression (2.2). When all considered indicators are of ratio scale, multidimensional poverty measures based on normalized deprivation gaps can be used. If the indicator is of interval scale, gaps may be redefined appropriately. When indicators are ordinal, measures based on normalized deprivation gaps are meaningless because results would vary under different admissible transformations of the indicators’ scales. The Adjusted Headcount Ratio presented in Chapters 5–10 can be meaningfully implemented using ordinal indicators, provided that issues of comparability are addressed as we will now clarify.

2.4 Comparability across People and Dimensions

The last section established the scales of measurement by which we can rigorously compare achievement levels in one variable, and the mathematical and statistical operations that can be performed on that variable. The discussion enabled us to identify the scale of measurement of each single indicator. Yet multidimensional measures seek to compare people’s achievements or deprivations across indicators, in ways that respect the scale of measurement of each indicator. This is by no means elementary. As Sen (1970) pointed out, cardinally meaningful variables may not necessarily be cardinally comparable—across people or, in multidimensional measurement, across dimensions. This section scrutinizes how these comparisons can legitimately proceed. That is, it takes a step back from the material presented thus far, to make explicit assumptions that have usually been implicit in work on multidimensional poverty measurement.

The issue of comparability across dimensions raised in this section has potentially significant empirical implications for quantitative methods beyond measurement. For example, as Chapter 3 will show, dichotomous data are regularly used in techniques that implicitly attribute cardinal meaning and comparability to the 0-1 values from several dimensions. If, in fact, the associated deprivation values of these data differ significantly from one another, then results based on techniques that treat each variable as cardinally equivalent may be affected; such exercises should, strictly, employ the 0-w variables because it is their relative weights or deprivation values that create cardinal comparability across dimensions. Hence the issues raised in this section, in a preliminary and intuitive way at this stage, have far-reaching implications for multidimensional analyses.

Multidimensional poverty measures, like income poverty measures, entail a basic assumption that the indicators are interpersonally comparable. Additionally, counting-based measures further assume that the same deprivation score is associated with the same level of poverty for different people. This assumption implies that deprivations have been made comparable. Comparability across dimensions must be obtained in order to generate cardinally meaningful deprivation scores and associated multidimensional poverty measures. But how? Multidimensional poverty measures may contain fundamentally distinct components that are not measured in the same units and may have no natural means of conversion into a common variable.

Empirically, the mechanics by which apparent comparability has been created in counting-based measures are clear (Chapter 4). When data are dichotomous and interpersonally comparable, the application of deprivation values is understood to create cardinal comparability across dimensions. When data are ordinal or ordered categorical, deprivation cutoffs are used to dichotomize the data; and those cutoffs, together with deprivation values, establish cardinal comparability across deprivations. In the case of appropriately scaled cardinal data, comparability across deprivations is created by the weights and the deprivation cutoffs.

Let us start with the most straightforward case: the deprivation matrix. This presents dichotomous values either because the original indicator is dichotomous (access to electricity), or because a cardinal, ordinal or ordered categorical variable has been dichotomized by the application of a deprivation cutoff into two categories: deprived and non-deprived.

A policy maker seeking to ameliorate poverty should have a good understanding of the various normative principles that her chosen poverty measure embodies, just as a pilot of a plane must have a sound understanding of how a particular plane responds to different operations. If the policy maker has a good understanding of the principles embodied by alternative measures then she will be able to choose the measure most closely reflecting publicly desirable ethical principles and most appropriate for the application—just as a pilot will choose the best way to fly the plane for a particular journey.

The first set of properties requires that a poverty measure should not change under certain transformations of the achievement matrix. We refer to these as

invariance properties, which are

symmetry,

replication invariance,

scale invariance and two alternative focus properties,

poverty focus and

deprivation focus. The second set requires poverty to either increase or decrease with certain changes in the achievement matrix. We refer to these as

dominance properties, which are

monotonicity,

transfer,

rearrangement, and

dimensional transfer properties. The third set of principles relates overall poverty to either groups of people or groups of dimensions and, thus is called

subgroup properties. Other properties, that guarantee that the measure behaves within certain usual, convenient parameters, we refer to as

technical properties. Each of the four following sections provides a formal outline and intuitive interpretations of each set of properties.

2.5.1 Invariance Properties

The first invariance principle is

symmetry. Symmetry requires that each person in a society is treated anonymously so that only deprivations matter and not the identity of the person who is deprived. Hence this property is also often referred to as

anonymity. As long as the deprivation profile of the entire society remains unchanged, swapping achievement vectors across people should not change overall poverty.

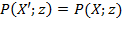

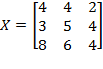

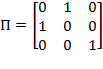

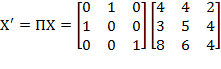

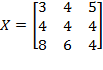

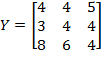

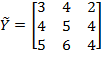

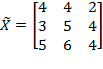

[74] This type of rearrangement can be obtained by pre-multiplying the achievement matrix by a permutation matrix of appropriate order.

Symmetry: If an achievement matrix

is obtained from achievement matrix

as

, where

is a permutation matrix of appropriate order, then

.

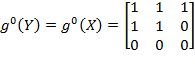

Example: Suppose the initial achievement matrix is

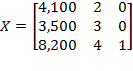

and the permutation matrix is

. Then:

. Note that the first and the second person (rows) in matrix

have swapped their positions. However, as long as the deprivation cutoffs remain unchanged, there is no reason for the level of poverty to be different for these two societies. Hence,

.

The second invariance principle,

replication invariance, requires that if the population of a society is replicated or cloned with the same achievement vectors a finite number of times, then poverty should not change.

[75] In other words, the replication invariance property requires the level of poverty in a society to be standardized by its population size so that societies with different population sizes are comparable to each other, as are societies whose populations change over time. Thus, this property is also known as the

principle of population.

[76]

Replication Invariance: If an achievement matrix

is obtained from another achievement matrix

by replicating

a finite number of times, then

.

Example: Suppose we are required to compare the level of poverty in two societies with the initial achievement matrices

and

. Note that the population sizes in these societies are different. In order to make them comparable, we replicate

twice to obtain

and

thrice to obtain

. By replication invariance, we know that

and

. Thus, it is equivalent comparing

to

and

to

.

The third invariance principle,

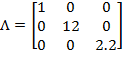

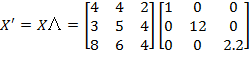

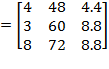

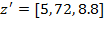

scale invariance[77] requires that the evaluation of poverty should not be affected by merely changing the scale of the indicators. For example, if the duration of completed schooling is an indicator, then deprivation in education, thus overall poverty, should be the same regardless of whether duration is measured in years or in months, provided the deprivation cutoff is correspondingly adjusted. The scale of any indicator in an achievement matrix can be altered by post-multiplying the achievement matrix by a diagonal matrix

of appropriate order (

, the number of dimensions). If a diagonal element is equal to one, then the scale of the respective indicator does not change. The diagonal elements of

need not be the same because different indicators may have different scales and units of measurement. A weaker version of the scale invariance principle, referred to as ‘unit consistency’, has been proposed by Zheng (2007) in the context of unidimensional poverty measurement and extended to the multidimensional context by Chakravarty and D’Ambrosio (2013). This principle requires that poverty comparisons, but not necessarily poverty values, should not change if the scales of the dimensions are altered.

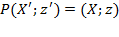

[78] The scale invariance property implies the unit consistency property, but the converse does not hold.

Scale Invariance: If an achievement matrix

is obtained by post-multiplying the achievement matrix

by a diagonal matrix

such that

, and the deprivation cutoff vector

is obtained from

such that

, then

.

Unit

Consistency: For two achievement matrices

and

and two deprivation cutoff vectors

and

, if

, then

Example: Suppose the initial achievement matrix is

and the deprivation cutoff vector is

. Matrix

is post-multiplied by the diagonal matrix

to obtain

. Similarly, vector

is post-multiplied by

to obtain

. Note that the first indicator and its deprivation cutoff did not change at all because the first diagonal element in

is 1. The second diagonal element in

is 12, as in 1 year = 12 months, and the third diagonal element in

is 2.2, as in 1 kilogram = 2.2 pounds. Scale invariance

requires that this transformation does not change overall poverty. Hence,

. Now suppose that there exists a hypothetical achievement matrix

such that

. Then, the unit consistency

property requires that the comparison does not change if both matrices and the vector

of deprivation cutoffs are multiplied by a diagonal matrix. Hence,

More formally, we say that

is obtained from

as an

equivalent representation if there exist appropriate admissible transformations

for

such that

and

for all

. In other words, an equivalent representation can comprise a set of admissible transformations, each of which is appropriate for each scale type, and which assigns a different set of numbers to the same underlying basic data. For example, an equivalent representation can include monotonic increasing transformations for ordinal variables, linear transformations for interval-scale variables, and proportional changes for ratio-scale variables. We now state the ordinality axiom as follows:

Ordinality: Suppose that

is obtained from

as an equivalent representation, then

.

Example: Suppose the initial achievement matrix is

and the deprivation cutoff vector is

, where the first dimension is measured with a ratio-scale indicator, say income in dollars

; the second dimension is measured with an ordinal-scale indicator, say self-rated health on a scale of one to five; and the third indicator is measured with a dichotomous 0-1 variable, say access to electricity. Suppose that income is now expressed in some other currency

, such that

(note that

in this case), self-rated health is now expressed with the scale (

and

) (note that

), and access to electricity is now coded as

for no access and

for access (i.e.

). Thus matrix

obtained from

is such that

, and

, then the ordinality property requires that

2.5.2 Dominance Properties

This section covers six principles, each of which has a stronger version and a weaker version. The stronger version requires that a poverty measure strictly moves in a particular direction, given certain transformations in the achievements of the poor. The weaker version, does not